Getty Images

Getty ImagesFalling mortgage rates may, at last, be bringing some relief to embattled homeowners and first-time buyers.

In a market described as “frenetic”, lenders are locked in intense competition for new customers while simultaneously trying to hold on to borrowers already on their books.

On supposedly unlucky Friday the 13th alone, big-name providers such as the Nationwide, HSBC and NatWest reduced their fixed rates. In an unusual move, TSB did so for the second time in a week.

Analysts expect further cuts to come, but brokers say the fear of missing out (FOMO) on better deals is paralysing some borrowers.

Failing to act before their current deal expires leaves them exposed to a much more expensive variable rate.

National obsession

During the last couple of years, mortgage rates have featured in discussions from chats around the dinner table to election debates.

About 1.6 million existing borrowers had relatively cheap fixed-rate deals expiring this year. Hundreds of thousands of potential first-time buyers have been hoping to get a place of their own.

Yet, rates have been volatile and much higher than what was the norm for more than a decade.

{kind=link}

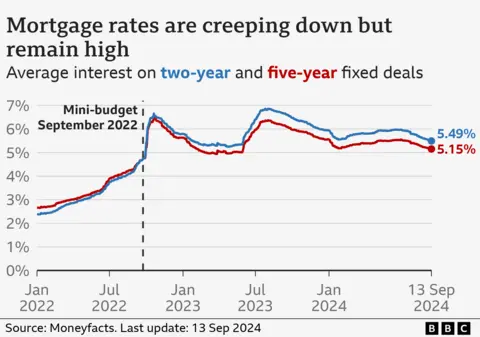

The interest rate on a fixed mortgage does not change until the deal expires, usually after two or five years, and a new one is chosen to replace it.

Average rates on new deals are now 5.49% for a two-year deal, the lowest for more than a year. Five-year deals have an average rate of 5.15%, according to the financial information service Moneyfacts.

However, the best, so-called headline, rates are reserved for those borrowing a small proportion of the value of the home (known as loan-to-value). A few are at levels not seen since rates shot up following the mini-Budget in the short-lived premiership of Liz Truss.

“Momentum is really starting to build now and the cuts are coming thick and fast.,” said Emma Jones, managing director at broker When The Bank Says No.

“Borrowers are the winners as lenders seek to compete for all-important market share as we head into the final months of the year.”

‘We took the plunge’

The Bank of England’s interest rate cut in August, with the potential for more to come, is part of the reason for falling mortgage rates.

That came slightly too late for Johnny and Sophie Abbott, whose last mortgage deal expired at the end of July.

Johnny Abbott

Johnny AbbottWhen they spoke to the BBC in March, the couple from Loughborough, who have three children, admitted every option seemed like a gamble.

In the end, they chose to buy a home that needed renovation.

“We took the plunge and can just about deal with the mortgage,” said Mr Abbott. “It will be great when it’s done.”

In June, the Bank of England said three million households would see their mortgage payments rise in the next two years, and about 400,000 mortgage holders were facing some “very large” payment increases.

A few months ago, Gary Rees expected to have to make serious lifestyle changes when his current deal expires in October. Now, things are looking better.

Yet, typical of many, the benefit is a smaller rise in his monthly mortgage repayments, not a fall. To be blunt, the financial punch won’t hurt as much.

“It’s improved, but my mortgage rate is still likely to double, rather than triple,” he said.

He is expecting to settle on a two-year deal, in the hope of further rate falls. The Bank of England’s next interest rate decision is on Thursday, although analysts are predicting a hold at 5%.

Getty Images

Getty ImagesThese two cases show that, although things are looking more positive for borrowers, not all are getting an equal benefit. Savers, meanwhile, are seeing the interest they receive worsen.

Brokers say that lenders have been offering the best deals to new, house-purchasing customers, rather than those who are remortgaging.

With relatively few buyers, providers are trying to get a piece of a small pie, according to David Hollingworth, of broker L&C. That includes offering loans at higher multiples of income, up to 5.5 times.

He said that while the lowest rates were “not divebombing”, the market was frenetic.

The market could also improve for remortgagers, he said, as lenders try to hit year-end targets.

Time to act?

Mr Hollingworth said the danger for any borrowers endlessly waiting for even lower rates to come is that they do nothing.

If a fixed deal expires, then borrowers automatically move on to their lender’s standard variable rate – which currently carries an average interest demand of 7.99%, which is two-and-a-half percentage points higher than a new two-year deal.

Adviser Jo Jingree, director of Mortgage Confidence, said people in the process of buying or remortgaging could still switch to a better deal if rates continued to fall before their personal deadline.

“I’ve seen first-hand that customers have been able to achieve revised mortgage offers on the lower rates which will save them money on their monthly payments,” she said.

Borrowers should monitor their rates, particularly a few weeks before their mortgage completes, to ensure they are getting the best possible rate, said Aaron Strutt, of broker Trinity Financial.

He expected rates to keep falling, especially if the Bank of England cuts the base rate on Thursday, or later this year.

With the cost of funding mortgages coming down, some in the industry suggest lenders could have cut rates more quickly.

They say lenders are making smaller price cuts week after week when they could be making larger reductions in one go.

Ways to make your mortgage more affordable

- Make overpayments. If you still have some time on a low fixed-rate deal, you might be able to pay more now to save later.

- Move to an interest-only mortgage. It can keep your monthly payments affordable although you won’t be paying off the debt accrued when purchasing your house.

- Extend the life of your mortgage. The typical mortgage term is 25 years, but 30 and even 40-year terms are now available.